Helicopter money coming to Japan? GMO on EU immigration and the Brexit. Hong Kong and China at a cross road. ECB coming up against its quantitative easing boundaries.

Headlines

Briefs

- China’s 2nd quarter gross domestic product came in at 6.7%, which is 10 basis points higher than forecast; however, the concern is where that growth has come from.

- “Figures from the People’s Bank of China the same day showed that money supply growth was faster than expected, reaching levels last seen post 2008. New loans also rose by over $200bn, more than $50bn higher than economists’ estimates.”

- Bottom line, “the reversion to state-led growth is unsustainable. Should China continue to shun reforms in favor of a quick fix, the short-term benefits of stabilized growth will be outweighed by the cost of persistent imbalances.”

- The World Federation of Advertisers “estimates that between 10 and 30% of online advertising slots are never seen by consumers because of fraud, and forecasts that marketers could lose as much as $50bn a year by 2025 unless they take radical action. At that scale, the fraud would rank as one of the biggest sources of funds for criminal networks, even approaching the size of the market for some illegal drugs.”

- “Global spending on online advertising has almost doubled in the past four years – reaching $159bn in 2015, according to research group eMarketer. This money underpins the internet economy and supports trillions of dollars of equity in media and technology.”

- “Google, the biggest player in the online ad industry, generated revenues of $67bn from it last year.”

- Bottom line, digital ad platforms and major buyers of online ads are emphatically building methods to track and prevent fraud and where they can and to the event that they can’t expect the federal government to step in.

- Mark Heschmeyer of CoStar reported on Simon, WP Glimcher turning over the keys on two malls to their respective lenders.

- Goes to show that just because a company is worth several billion dollars, doesn’t mean they pay back all their debts.

- “While the overall retail property sector appears to be strengthening, a handful of loans for lower-quality shopping centers and malls financed at the height of the previous CRE cycle are coming due now and proving to be a thorn in the side of publicly traded REITs.”

- “Simon Property Group and WP Glimcher both turned malls back over to the lenders this week, and Kimco Realty Corp. disclosed that it doesn’t expect one of its joint venture-owned malls will be able to refinance a loan set to come due this fall.”

- “All three of the malls involved in the foreclosure actions were last financed in 2006 and securitized in mortgage backed bond conduits.”

- As the saying goes, don’t hate the player, hate the game.

Special Reports

- Bloomberg – The Fake Factory That Pumped Out Real Money – Mario Parker, Jennifer A. Dlouhy, & Bryan Gruley 7/13

- Entertaining read on a bio-diesel fraud to the tune of $100m.

- DiMartino Booth – The Bond Market: Beware of Junkyard Dogs – Danielle DiMartino Booth 7/20

- “Defaults are going through the roof and investors are flocking to the sector in record numbers?”

- Knowledge@Wharton – How Venezuela Fell Apart 7/12

- “In 1950, when the global economy was struggling to recover from World War II, oil-rich Venezuela was the world’s fourth-wealthiest country, boasting a per capita GDP of $7,424 exceeded only by the United States, Switzerland and New Zealand. Indeed, Venezuela’s per capita income was nearly four times that of Japan (at $1,873), nearly twice that of Germany ($4,281) and more than 12 times that of China ($614), according to NationMaster.com, an economics statistics site. By 2012, Venezuela’s per capita GDP ranked 68th in the world, according to the World Economic Forum. But it has continued to shrink since then, dropping 5.7% in 2015 and by a projected 7.1% rate in 2016, according to the country’s central bank. Inflation in Venezuela, the highest in the world, reached 159% in 2015 and is expected to grow to 204% this year, according to the International Monetary Fund.”

- Mauldin Economics – You Can Polish a Turd, But You Can’t Make It Shine – Jared Dillian 7/14

- Basically, it’s going to be tough to fight deflation in Japan when the country’s population is shrinking.

Graphics

FT – Do sovereign credit ratings still matter? 7/14

FT – US oil rig count rises for third-straight week 7/15

FT – Auto sales and the oil price: the Great Unwinding continues beyondbrics – Paul Hodges 7/18

Temporary work – How the 2% lives: Temping is on the increase, affecting temps and staff workers alike

FT – Independent Chinese PMI gauge suspended indefinitely – Hudson Lockett 7/20

Featured

*Note: bold emphasis is mine, italic sections are from the articles.

Japan flirts with helicopter money. Gavyn Davies. Financial Times. 17 Jul. 2016.

“Whether or not they choose to admit it the Abe government is on the verge of becoming the first government of a major developed economy to monetize its government debt on a permanent basis since 1945.”

“There are many ways of defining helicopter money, but the essential feature is that it involves an increase in the budget deficit which is financed by a permanent increase in the central bank’s monetary base, not by the issuance of government debt.”

“This is different from quantitative easing, since QE involves the ‘temporary’ purchase of government debt, which is subsequently sold back into the market, at least in theory. And QE does not necessarily need to involve any increase in the budget deficit…”

While “the direct financing of a government deficit by the Bank of Japan is illegal, under Article 5 of the Public Finance Act.” It looks like the government is coming up with a work-a-round.

One method proposed is the issuance of perpetual bonds “…which basically involves the central bank printing money and giving it to the government to spend as it chooses. There would be no buyers of this debt in the open market, but it could presumably sit on the BoJ balance sheet forever at face value.”

Thing is, that “there is no doubt that the BoJ is now monetizing much of the increase in government debt needed to fund ¥10 trillion fiscal stimulus planned by the government. Since the market fully expects the BoJ’s debt purchases to be permanent, it is helicopter money by any other name.”

Why do this when the labor market is at close to full employment? Basically the inflation expectations in Japan are REALLY low and the BoJ is seeking to reduce its vulnerability to “…any new deflationary shock, from China for example.”

The key point that helicopter money will confer is that debt sustainability (which is why the sales tax increases have been/are being implemented) is not the priority. Rather that Japan will live with whatever debt level it takes to achieve inflation.

“The key problem is that it might restore inflation far too well. It is very difficult to calibrate the amount of helicopter money that is needed to hit the inflation target.”

Expect the delicate dance to continue, which may fail to get Japan out of its deflationary rut.

Immigration and Brexit. Jeremy Grantham. GMO. Jul. 2016.

While this is piece is a commentary on immigration and the Brexit, I think it does a good job of presenting the scale of the immigration challenge that the EU is facing. I will only highlight two specific items (the full commentary is a good read) for brevity. 1) Grantham’s stance on the markets “despite brutal and widespread asset overpricing, there are still no signs of an equity bubble about to break…” and 2) some of his thoughts on immigration to the EU.

“The truth about immigration to the EU, in my view, is bitter. As covered in earlier quarterlies, I believe Africa and parts of the Near East are beginning to fail as civilized states.”

“They are failing under the pressure of populations that have multiplied by 5 to 10 times since I was born; climate for growing food that is deteriorating at an accelerating rate; degraded soils; insufficient unpolluted water; bad governance; and lack of infrastructure. Country after country is tilting into rolling failure.”

“This is producing in these failing states increasing numbers of desperate people, mainly young men, willing to risk money and their lives to attempt an entry into the EU.”

“For the best example of the non-compute intractability of this problem, consider Nigeria. It had 21 million people when I was born and now has 187 million. In a recent poll, 40% of Nigerians (75 million) said they would like to emigrate, mostly to the UK (population of 64 million). Difficult. But the official UN estimate for Nigeria’s population in 2100 is over 800 million! (They still have a fertility rate of six children per woman). Without discussing the likelihood of ever reaching 800 million, I suspect you will understand the problem at hand. Impossible.”

“I wrote two years ago that this immigration pressure would stress Europe and that the first victim would be Western Europe’s liberal traditions. Well, this is happening in real time as they say, far faster than I expected. It will only get worse as hundreds of thousands of refugees becomes millions.”

Hong Kong: One country, two economies. Ben Bland. Financial Times. 19 Jul. 2016.

Integration of Hong Kong with the Chinese mainland continues to be a delicate issue that is being stressed by a slowdown in the Chinese economy.

As Lily Lo, an economist at DBS, a Singaporean bank, put it “Hong Kong is really dependent on China and external trade. The Chinese economy is slowing down and this is a structural slowdown so we don’t think there will be a V-shaped recovery any time soon. There’s no quick fix.”

Further, as China has opened its economy more and more, Hong Kong is no longer the only or primary route to do business with China. “Its container port, which was the world’s busiest in the 2000s, has fallen to fifth place, overtaken by Shanghai, Shenzhen and Ningbo.”

“Mr. Tsang (John Tsang, the financial secretary of Hong Kong) and Li Ka-shing, the billionaire whose interests in Hong Kong stretch from ports to property and retail to telecoms, have both warned that the economic outlook is worse than that faced during the Sars epidemic in 2003, which killed 299 people and prompted the last sharp slowdown.”

“Chow Tai Fook, the biggest jeweler in the world by market capitalization, is seen as a bellwether for mainland demand for Hong Kong’s luxury goods. Its sales in Hong Kong and Macau fell on an annualized basis by 22% in the three months to the end of June.”

“Yu Kam-hung, managing director of investment properties at CBRE, an estate agent, predicts that prices could fall up to 10% over the next year, and they are already 10 to 15% off their peak of 18 months ago.”

Then of course it doesn’t help that “there is a deep-seated animosity to (Chinese) mainlanders in Hong Kong. So why would they want to go somewhere they are not welcome when there are so many other choices.” – Shaun Rein, China Market Research in Shanghai

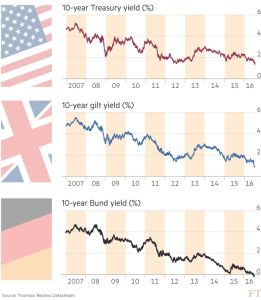

ECB faces QE dilemma after Brexit vote. Claire Jones and Elaine Moore. Financial Times. 20 Jul. 2016.

It wasn’t long after the Brexit referendum vote that government bond yields in the safest markets dropped even further (see graphic on Sovereign credit ratings above). Problem is that the current structure in place within the European Central Bank (ECB) is reaching its limits.

Currently the ECB is buying €80bn a month in European member country debt to stimulate the overall European economy (aka Quantitative Easing or QE).

Well, “under current rules, the scale of purchases under QE match the size of a member state’s economy, meaning that Germany’s Bundesbank must buy around €10bn of government debt each month – more than any other central bank in the region.”

“But because of the recent bond market shifts, more than 50% of German bonds previously eligible for QE have now become too expensive for the Bundesbank to purchase, yielding less than the ECB’s self-imposed floor of minus 0.4%, according to data from Bank of America Merrill Lynch.”

So, now the ECB is essentially faced with three primary options (there are other options – see “Five ways to change the rules within the article).

- Scrap the minus 0.4% floor. The “economists at Goldman Sachs calculate (this) would buy the ECB the most time, enabling the Bundesbank to keep buying for up to another 18 months.”

- “The option, however, would expose the eurozone’s central banks to heavy losses, which they have until now avoided because the minus 0.4% floor mirrors the ECB’s deposit rate charged on banks’ reserves.”

- “Scrap the rule that bond purchases match the size of a member states’ economy.”

- “But such a shift would open the way to buying more bonds from the most indebted countries, and would so be the most controversial of the fixes. Nowhere would it attract more criticism in Germany, where the change would be viewed as a bailout by the back door for profligate member states.”

- End QE.

Don’t know if the EU or the world is ready for that.

Other Interesting Articles

Bloomberg Businessweek

The Economist

Bloomberg – Blackstone Said to Plan Invitation Homes IPO for First Half 2017 7/17

CoStar – Internet Commerce Drives Strongest Surge in Demand for US Industrial Space Since 2001 7/20

FT – The chronic spin that blights China’s economy 7/14

FT – New wealth management products power Anbang and rivals 7/17

FT – Major cities drive China property price gains 7/17

FT – Trump leads the west’s flight from dignity 7/17

FT – Apple Watch sales fall 55% as consumers mark time on category 7/21

InvestmentNews – REIT with a twist – and a high commission – is new darling of independent brokers-dealers 7/14

NYT – The Risk of Building on Real Estate Funds’ Profitable Past 7/15

NYT – Why Land and Homes Actually Tend to Be Disappointing Investments 7/15

NYT – Vast Purge in Turkey as Thousands Are Detained in Post-Coup Backlash 7/18

WSJ – Surprise: The Economy Is Looking Much Better 7/14

WSJ – China Economy Tilts Further in Wrong Direction 7/15

WSJ – Japan and Helicopter Money: Fan Blades Aren’t Turning Just Yet 7/17

WSJ – Big Chinese Developers Push Into Hong Kong Market 7/19