The $860bn gorilla is increasing its real estate allocation, Saudi Arabia wants to borrow money, and Passport Global’s commentary on QE, China, and illiquidity.

This week three articles that stood out were 1) Saleha Mohsin’s two-part article in BloombergBusiness “Norway SWF Says Adding $86 Billion in Properties May Be Best” and “Norway’s Wealth Fund Targets Major Cities After Bonds Hit Zero” that covered Norway’s sovereign wealth fund’s planned increase in real estate allocations, 2) was Simeon Kerr’s “Saudi Arabia to tap global bond markets as oil fall hits finances” in The Financial Times that pointed out that Saudi Arabia is about to tap the international debt markets for the first time, and 3) was posting in ValueWalk “Passport Global Up 6.7% in Q3; Burbank Worries About Liquidity” by Rupert Hargreaves that was a commentary of Passport Global’s portfolio positions.

*Note: bold emphasis is mine, italic sections are from the articles.

Norway SWF Says Adding $86 Billion in Properties May Be Best. Saleha Mohsin. BloombergBusiness. 5 Nov. 2015.

Norway’s Wealth Fund Targets Major Cities After Bonds Hit Zero. Saleha Mohsin. BloombergBusiness. 5 Nov. 2015.

Basically the world’s biggest sovereign wealth fund ($860bn) has had back-to-back quarterly losses. The first time in six years.

“The fund lost 273 billion kroner ($32 billion) in the third quarter, or 4.9%, amid a drop in global stocks. Its stock holdings declined 8.6%, while it posted a 0.9% gain on bonds and a 3% return on real estate.”

“…The fund’s annual real return has been 3.55% since 1998, behind a government target of 4%.”

The fund isn’t really reaching for yield at a 4%, but

“Slyngstad (CEO) says record-low interest rates will make it difficult to meet return targets in the years ahead.”

While…

“The fund said that nominal returns on real estate have averaged about 7% to 9% from 2000 to 2013 but have seen a “declining trend in recent years.””

And…

“The vast majority of academic studies come to the conclusion that adding real estate does improve the risk-return profile of a mixed-asset portfolio,” the fund said in a discussion note based on research released on Friday. “Estimates of optimal allocations to real estate vary strongly. The median range of the suggested allocations to real estate in the 30 studies reviewed was 15%.”

Therefore,

“Norges Bank Investment Management, which oversees the fund from within the central bank, held about 3% of its assets in real estate at the end of the third quarter. It aims to build that share to 5% by investing about 50 billion kroner ($5.8 billion) each year in property. The investor has a strategy to focus on 10 to 15 cities globally.”

And the fund is even considering raising their allocation to 15%, an additional $86bn that would be funneled in to real estate. I’m sure they’re not the only ones. The implications should assist real estate valuations even if the Fed does raise rates in December. Basically, cap rates will hold and the spreads over treasuries will shrink.

Saudi Arabia to tap global bond markets as oil fall hits finances. Simeon Kerr. The Financial Times. 9 Nov. 2015.

As low oil prices linger on Saudi Arabia has found itself in a new position of raising debt. While the Kingdom has plenty of reserves on hand (unlike Russia and Venezuela), the country is raising debt while it is cheap to cover their shortfalls that exists due to extensive social programs/commitments to its citizens.

“The decision to tap bond markets underscores the impact on the kingdom’s revenues from the plunge in the oil price, from $115 a barrel last year to $50 now, as well as Riyadh’s expensive military intervention in Yemen.”

To highlight how new this is,

“The authorities are in the meantime looking to set up a debt management office to help oversee the process of raising local and international bonds.”

While some domestically held debt has been issued, this their first time taping international markets and debt levels may increase to as much as 50% of GDP within 5 years (6.7% in 2015 and 17.3% in 2016).

“Riyadh started to issue domestic bonds in the summer to fund its budget deficit. The government could continue to issue domestically for another 12 to 18 months, officials say, but it will need to diversify globally to leave liquidity available for private sector lending.”

As a reminder,

“Over the past year, Saudi Arabia has seen its foreign reserves decline from last year’s high of $737bn to a three-year low of $647bn in September.”

Thus,

“Standard & Poor’s last month reduced Saudi Arabia’s ratings from ‘AA-/A-1+’ to ‘A+/A-1’, saying it could lower them again “if the government did not achieve a sizeable and sustained reduction in the general government deficit.”

But Moody’s did not change its Aa3 stable rating.

Passport Global Up 6.7% in Q3; Burbank Worries About Liquidity. Rupert Hargreaves. ValueWalk. 6 Nov. 2015.

In this posting Hargreaves provides a review of Passport Global’s third quarter results and brings up Passport’s outlook. What really stood out to me were the following excerpts from Passport:

“Passport goes on to report that tensions have built up in the global financial system since the Fed initiated QE in 2009:

“The coupling of low U.S. interest rates and asset purchases by the Fed put downward pressure on the U.S. dollar and created the backdrop for a carry trade as interest rates and expected returns were higher in foreign domiciles. However, as experienced in past carry trades, while growth can benefit substantially in the run-up, the unwind can leave lasting scars.”

“The corporate debt of non-financial firms in the largest emerging market economies has more than quadrupled from $4 trillion in 2004 to in excess of $18 trillion in 2014, according to the International Monetary Fund (IMF). Approximately a quarter of bond issuances were done in foreign currency and requires annual servicing costs in excess of $236 billion USD.”

“Along with the prospect of rising interest rates in the U.S., we see the repayment and servicing of this debt to be more straining on emerging market corporates. Simultaneously, we see the U.S. dollar becoming more scarce as petro-dollars and revenues generated from commodities priced in dollars have cratered. The world isn’t being supplied with U.S. dollars at the level it has become accustomed to over the past seven years. The U.S. current account deficit continues to decline, 7.3% from 1Q15 to 2Q15. If the Fed keeps on its current path of raising interest rates, we believe U.S. dollar liquidity around the world will only continue to fall.”

“On China as a risk to markets:

“We believe the big risk for global markets over the next several months is a worsening in China’s economy characterized by non-performing loan (NPL) issues—which could lead China to de-peg from the U.S. dollar, lower rates and, in the process, force the liquidation of risk assets around the world. In our view, investors should prepare for a worsening global economic environment and the potential for recessions in both the U.S. and globally.”

“On market illiquidity:

“Market illiquidity, by our measure, is only getting worse. That has led us to run with a lower gross and a low net exposure. The long U.S. dollar trade is still at work. However, we have to work through all those participants who were assuming the Fed would hike because of strong U.S. growth, and we don’t know how long that’s going to play out. U.S. equities and the S&P 500 in particular appear much safer than emerging market equities and those of most other developed markets around the world.”

Brace yourselves.

Other Interesting Articles

The Economist

AWC: Are The Private Markets Getting Too Crowded? 11/12

BloombergBusiness: Goldman Sachs Sees 60% Chance U.S. Expansion Lives to See Ten 11/9

FT: Low oil lifts credit risk at US banks 11/5

FT: Square IPO: payments group prices shares below private market 11/6

FT: Grasp the reality of China’s rise 11/8

FT: Only a crisis can stop the Federal Reserve 11/6

FT: New York art auction sounds gloomy note 11/9

FT: US is suffering a profits recession 11/9

FT: Oil glut to swamp demand until 2020 11/10

FT: US corporate bond yields near 2013 peak 11/11

NYT: The Mystery of the Vanishing Pay Raise 10/31

NYT: Dizzying Ride May Be Ending for Tech Start-Ups 11/10

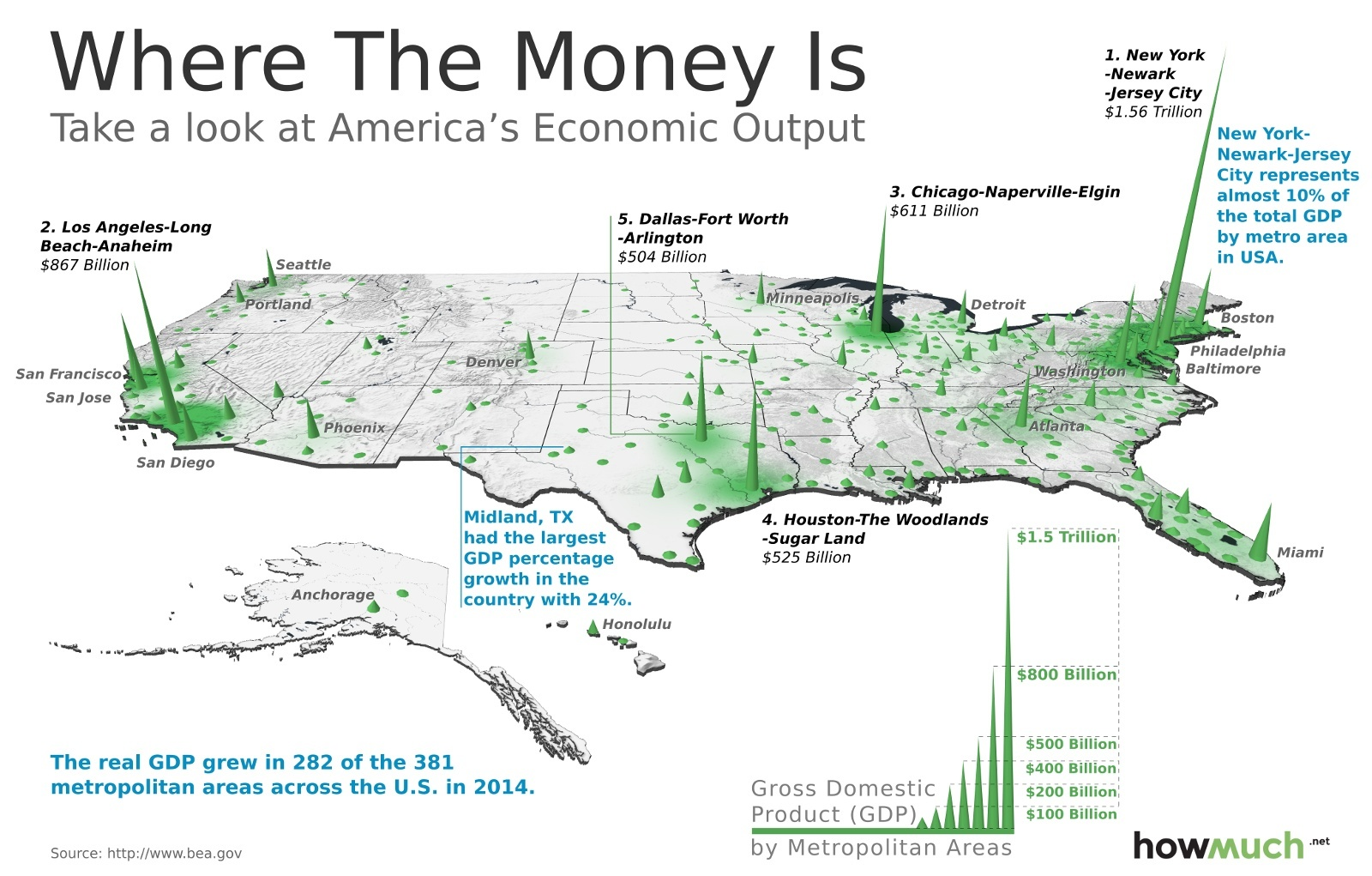

The Big Picture: “Where The Money Is – Take a look at America’s Economic Output” – howmuch.net 11/6

{kind=link}

WP: Baby boomers are what’s wrong with America’s economy 11/5

WSJ: Apollo’s Deal for Control of Schorsch Real-Estate Empire Falls Apart 11/8

WSJ: What $1.5 Trillion in Stock Buybacks Doesn’t Buy 11/8

WSJ: Takeover Loans Have Few Takers on Wall Street 11/8

WSJ: London Office Development Hits Highest Level in Seven Years 11/10

WSJ: Rental Portion of One57 Is For Sale 11/10

WSJ: China Learns What Pushing on a String Feels Like 11/12